Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 28 / What to expect Jan 13, 2025 thru Jan 17, 2025

In This Issue

Market-On-Close: All of last week’s market-moving news and macro context in under 5 minutes + futures-snapshots

Special Coverage: Getting Defensive with Personal Portfolios in a Volatile Environment

The Latest Investor Sentiment Readings

Institutional Support & Resistance Levels For Major Indices: Exactly where to look for support and resistance this week in SPY, QQQ, IWM & DIA

Institutional Activity By Sector: Institutional order flow by sector including the top institutionally-backed names in those sectors. We break it all down and provide the key insights and take-aways you need to navigate institutional positioning this week.

Top Institutional Order Flow In Individual Names: All of the largest sweeps and blocks on lit exchanges and hidden dark pools

Investments In Focus: Bull vs Bear arguments for FVRR, HDB, RDY, VV, RGTI, SAP

Top Institutionally-Backed Gainers & Losers: An explosive watchlist for day traders seeking high-volatility

Normalized Performance By Thematics YTD (Sector, Industry, Factor, Energy, Metals, Currencies, and more): which corners of the markets are beating benchmarks, which ones are overlooked and which ones are over-crowded

Key Econ Events and Earnings On-Deck For This Week

Market-On-Close

Shifting Tides: U.S. Financial Markets Face Reality Check Amid Strong Economic Data

The second week of January 2025 has delivered a stark reality check to financial markets, forcing investors to confront a fundamental disconnect between their optimistic rate cut expectations and the persistent strength of the U.S. economy. As major indices retreated from their recent highs, with the S&P 500 and Dow Jones Industrial Average both falling to two-month lows, the market narrative has shifted dramatically from when the Federal Reserve might cut rates to whether such cuts are even warranted in the current economic environment.

The catalyst for this reassessment came from Friday's remarkably robust employment report, which showed the U.S. economy added 256,000 jobs in December, substantially exceeding consensus expectations of 165,000. This demonstration of labor market resilience, coupled with an unexpected drop in the unemployment rate to 4.1%, has complicated the Federal Reserve's path forward. While strong employment typically signals economic health, in the current context it presents a complex challenge for monetary policy makers attempting to navigate the final mile of their inflation fight.

The market's reaction to this strong economic data was swift and decisive. Treasury yields surged, with the benchmark 10-year yield climbing to 4.786%, its highest level in 14 months. This sharp move in yields reflects a fundamental repricing of rate cut expectations, with market participants now discounting the probability of a January rate cut to a mere 3%. The ripple effects of this reassessment were felt across asset classes, leading to particularly pronounced weakness in growth stocks and other rate-sensitive sectors.

Adding to these concerns, the University of Michigan's consumer sentiment survey revealed a troubling uptick in inflation expectations. The jump in both short-term and long-term inflation expectations to 3.3% suggests that despite the Federal Reserve's aggressive tightening campaign, inflationary pressures may be becoming more deeply entrenched in economic behavior and expectations. This development is particularly worrisome for Federal Reserve officials, who view inflation expectations as a crucial indicator of their policy effectiveness.

The technology sector, which had led the market's recent advance, faced additional headwinds beyond just higher rates. Reports that the Biden administration is considering new restrictions on AI chip sales introduced another layer of uncertainty for semiconductor stocks. Industry leaders like Nvidia and AMD saw their shares decline significantly, with AMD facing additional pressure from a Goldman Sachs downgrade. This regulatory uncertainty, combined with elevated valuations and rising yields, has caused investors to reassess their positioning in the sector that had been the market's primary driver.

However, not all sectors succumbed to the selling pressure. Energy stocks demonstrated relative strength as crude oil prices reached three-month highs. Companies like Coterra Energy, Devon Energy, and Diamondback Energy posted gains exceeding 2%, suggesting that investors are beginning to position for a potential environment of sustained economic strength rather than the slower growth scenario that had been previously priced into markets.

The fixed income markets have perhaps seen the most dramatic shift in sentiment. Beyond the move in Treasury yields, corporate bond spreads have widened, reflecting growing concern about the impact of higher-for-longer rates on corporate borrowing costs. The international bond markets have not been immune to these pressures, with German bund yields reaching six-month highs and UK gilt yields touching levels not seen in decades.

This market environment marks a significant departure from the euphoric conditions that characterized the end of 2024. The combination of strong economic data and persistent inflation concerns has forced investors to confront the possibility that the Federal Reserve's restrictive monetary policy stance may need to remain in place longer than previously anticipated. This reassessment is occurring against a backdrop of historically high valuations, particularly in the technology sector, creating a potentially volatile mix for markets.

Looking ahead, several key catalysts could determine the market's direction in the coming weeks. The start of fourth-quarter earnings season will provide crucial insight into corporate America's ability to maintain profitability in a higher-rate environment. The upcoming Consumer Price Index report will be closely watched for signs of whether December's strong wage growth is translating into broader inflationary pressures. Additionally, markets will be particularly attuned to any shifts in Federal Reserve communication that might signal a change in their policy stance.

For investors, this environment demands a more nuanced approach than the relatively straightforward strategies that worked in 2024. The market's reaction to strong economic data suggests that good news for the economy might not necessarily translate into good news for asset prices, particularly if it leads to a longer period of restrictive monetary policy. This dynamic argues for increased attention to valuation and quality factors in portfolio construction.

The recent market action also highlights the importance of maintaining appropriate diversification across sectors and asset classes. While technology stocks have dominated returns in recent years, the current environment may favor a broader approach that includes exposure to both growth and value sectors. The strong performance of energy stocks amid market weakness serves as a reminder that different sectors can provide valuable portfolio diversification benefits in changing market conditions.

The fixed income market's dramatic moves suggest that bonds may finally be returning to their traditional role as a source of both income and potential portfolio protection. The higher yields now available across the fixed income spectrum offer investors more attractive entry points, though careful attention to duration risk remains warranted given the uncertain path of monetary policy.

As we progress through 2025, markets appear to be entering a new phase where the easy assumptions about Federal Reserve policy and market direction that characterized much of 2024 are being challenged. This environment demands a more disciplined approach to investment decision-making, with increased attention to fundamentals, valuation, and risk management. While the strong economic data suggests the U.S. economy remains on solid footing, the path forward for markets may be more challenging than many investors had anticipated at the start of the year.

The coming weeks will be crucial in determining whether the current market weakness represents a healthy correction in an ongoing bull market or the start of a more significant adjustment to higher-for-longer interest rates. Either way, investors would be wise to prepare for an environment of increased volatility as markets digest the implications of continued economic strength and its impact on monetary policy expectations.

Futures Markets Snapshots

S&P 500: Sector Insights

Technology

Microsoft ( MSFT 0.00%↑ +0.09%): Flat performance reflects investor caution despite optimism around cloud services. The slowdown in broader tech is currently hampering upside.

Oracle ( ORCL 0.00%↑ -6.95%): Significant declines linked to earnings that missed expectations continue to weigh on price, driven by slowing cloud revenue growth as competitors like Microsoft and Amazon gain market share. Ex-dividend was Friday the 10th.

Nvidia ( NVDA 0.00%↑ -1.74%): Declined after weeks of strong gains as investors rotated out of high-growth AI names into value sectors. Profit-taking also played a role.

Advanced Micro Devices ( AMD 0.00%↑ -3.81%): Under pressure from mixed analyst reports suggesting rising competition in the semiconductor market. Mizuho cut its price target to $160.

Consumer Cyclical

Tesla ( TSLA 0.00%↑ +4.08%): Gained after announcing strong delivery numbers and optimism around new EV product launches, including the Cybertruck.

Amazon ( AMZN 0.00%↑ -0.58%): Marginal losses as the e-commerce giant continues to face scrutiny over slowing retail growth and rising costs in its logistics network.

Communication Services

Alphabet ( GOOG 0.00%↑ +1.33%): The company outperformed on optimism around its AI capabilities and growing market share in digital advertising.

Meta Platforms ( META 0.00%↑ +2.77%): Gains were supported by better-than-expected adoption of its Threads platform and advertising rebound in key markets.

Netflix ( NFLX 0.00%↑ -5.53%): Declined as concerns about subscriber growth surfaced, driven by intensifying competition in the streaming industry.

Healthcare

Eli Lilly ( LLY 0.00%↑ +2.81%): Strong gains were tied to positive drug trial results and optimism around its diabetes and obesity treatments.

UnitedHealth Group ( UNH 0.00%↑ +3.21%): The stock rose this week, driven by optimism around its Medicare Advantage enrollments, bolstered by positive sentiment from recent industry trends and an analyst upgrade highlighting its strong competitive positioning in the managed care space

Industrials

General Electric ( GE 0.00%↑ +1.84%): Continued strength in its aerospace division, bolstered by demand for jet engines, helped the stock outperform.

Boeing ( BA 0.00%↑ -2.24%): Declined due to reports of ongoing production delays affecting key aircraft models.

Consumer Staples

Walmart ( WMT 0.00%↑ +3.33%): Outperformed as consumer demand for value shopping remains resilient in the face of inflationary pressures.

Procter & Gamble ( PG 0.00%↑ -4.47%): Declined due to concerns over slowing demand for consumer goods as discretionary spending tightens.

Energy

Chevron ( CVX 0.00%↑ +4.38%): Strong gains followed a rebound in crude oil prices, supported by tighter OPEC production quotas.

ExxonMobil ( XOM 0.00%↑ -0.72%): Marginal losses may reflect concerns over its refining margins despite strong oil prices and little in the way of news this week.

Financials

JP Morgan ( JPM 0.00%↑ -0.05%): Flat performance reflects a balance between strong deposit growth and concerns about higher funding costs impacting net interest margins ahead of earnings from a number of Financial-names starting next week

Bank of America (BAC, +1.95%): Benefited from investor optimism over rising interest rates improving margins on lending portfolios ahead of earnings on the 16th.

Utilities

Duke Energy ( DUK 0.00%↑ -5.71%): Declined sharply as rising Treasury yields make dividend-paying stocks less attractive to income-focused investors. Duke held its quarterly dividend at $1.045/share but the downside-surprise in earnings back in Nov is still weighing on the stock.

Key Takeaways

Technology Weakness: Continued selloff in tech names like Oracle and Nvidia reflects broader market caution around high valuations.

Healthcare Strength: Gains in healthcare were driven by company-specific catalysts, including positive drug trials (Eli Lilly) and robust enrollments (UnitedHealth) and possibly indicate rotation into defensives.

Energy Rebound: The sector was buoyed by rising oil prices and OPEC-led production cuts, benefiting Chevron significantly.

Consumer Staples Underperformed: Household goods names like Procter & Gamble struggled under slowing consumer spending trends.

ETF Insights

US Large Cap

SPY (-0.71%) and QQQ (-0.60%): Both broad-market ETFs saw marginal declines, driven by continued rate-sensitive rotations out of growth stocks, though losses were relatively muted this week.

RSP (-0.84%): The equal-weighted S&P 500 ETF slightly underperformed SPY, reflecting continued struggles in smaller names and more even distribution of weakness across sectors.

US Sector ETFs

Technology (XLK, -1.38%): The technology sector remained under pressure due to rate concerns impacting valuations. However, leveraged bear ETF SOXS (-3.33%) declined, suggesting some recovery in semiconductors, while SOXX (+0.64%) gained modestly as certain chip stocks rebounded.

Healthcare (XLV, +1.48%): Outperformed due to continued strength in managed care providers and biotech names. This was supported by defensive positioning amidst macro uncertainty.

XBI (-2.28%): Biotech-focused ETFs underperformed relative to broader healthcare due to specific regulatory and funding concerns in smaller biotech names.

Energy (XLE, +2.00%): The energy sector led gains, supported by a rebound in crude oil prices.

XOP (+3.33%): Outperformed within energy, reflecting strong momentum in oil exploration and production stocks.

Consumer Discretionary (XLY, -0.26%): Marginal declines reflect ongoing consumer spending concerns. Homebuilders like ITB (-1.37%) remained under pressure amid rising mortgage rates.

Small and Mid-Cap ETFs

IWM (-1.95%) and MDY (-0.47%): Small- and mid-cap ETFs underperformed as rising borrowing costs and tightening credit conditions weighed on smaller, more rate-sensitive companies.

Leveraged bear small-cap ETF TZA (+6.02%) surged, reflecting bearish sentiment in the segment.

Global and International ETFs

China ( FXI 0.00%↑ , -4.15%): Chinese ETFs posted significant losses as weak economic data and geopolitical tensions weighed on sentiment.

Leveraged bull ETF YINN (-12.49%) was particularly hard-hit, reflecting continued bearishness in Chinese equities.

Emerging Markets ( EEM 0.00%↑ , -1.60%): Declined broadly as a stronger dollar and global growth concerns put pressure on developing economies.

Japan ( EWJ 0.00%↑ , -2.64%): Japanese ETFs fell, reversing some recent strength, as concerns over global growth began to weigh on industrial and export-heavy economies.

Fixed Income

TLT 0.00%↑ (-2.41%): Long-duration Treasury ETFs declined as bond yields continued to rise amidst fears of higher-for-longer interest rates.

Leveraged long Treasury ETF TMF (-7.35%) saw outsized losses due to its sensitivity to rising rates.

IEF 0.00%↑ (-1.26%): Intermediate-term Treasuries also struggled, reflecting broader fixed-income challenges.

Commodities

Gold ( GLD 0.00%↑ , +1.14%) and Silver ( SLV 0.00%↑ , +2.52%): Precious metals rebounded this week as safe-haven demand picked up amidst economic uncertainty and geopolitical risks.

Crude Oil ( USO 0.00%↑ , +6.55%): Oil ETFs surged on the back of tightening OPEC production cuts and geopolitical concerns, further lifting energy-related ETFs.

Leverage and Inverse ETFs

SOXL 0.00%↑ (-1.41%) and SOXS (-3.33%): Mixed performance in leveraged semiconductor ETFs reflects ongoing volatility in the chip space, with some stabilization this week.

TNA 0.00%↑ (-6.08%): Leveraged bullish small-cap ETF suffered significantly as smaller companies remained under pressure.

TZA 0.00%↑ (+6.02%): Small-cap bear ETFs rallied on the back of weak sentiment in the small-cap segment.

Cryptocurrency ETFs

BITO 0.00%↑ (-2.91%): Crypto ETFs fell slightly as Bitcoin retraced some recent gains, reflecting profit-taking and regulatory concerns.

GBTC 0.00%↑ (-2.76%): Similarly declined as the market consolidated after a strong rally in prior weeks.

Key Takeaways

Energy Leads the Market: The energy sector was the standout performer, with crude oil prices surging, benefiting ETFs like XLE 0.00%↑ and XOP 0.00%↑ .

China Weakness: Chinese ETFs were among the worst performers due to weak economic data and geopolitical headwinds, dragging down FXI 0.00%↑ and YINN 0.00%↑ .

Fixed Income Under Pressure: Rising bond yields continued to weigh on fixed-income ETFs, with long-duration Treasury ETFs like TLT 0.00%↑ and TMF 0.00%↑ seeing notable declines.

Small-Cap Struggles Persist: Small-cap ETFs significantly underperformed, reflecting heightened sensitivity to rising borrowing costs and credit conditions.

Special Coverage: Getting Defensive with Personal Portfolios in a Volatile Environment

The financial markets are inherently cyclical, oscillating between periods of growth and contraction. Certain moments, however, heighten the risk of volatility: political transitions, economic uncertainty, or macroeconomic shocks. In such an environment, investors often struggle to preserve capital while remaining positioned for future opportunities. Recent trends—such as the consolidation and subsequent sell-off in sectors like Consumer Staples (XLP) and a notable uptick in the VIX—signal the need for a more defensive approach to portfolio management.

This written piece explores how investors can position themselves defensively in a volatile market. We'll examine historically resilient sectors, portfolio instruments designed to reduce risk, and strategies for preserving cash to redeploy under more favorable conditions. Through these insights, investors can better navigate turbulent markets while maintaining long-term financial goals.

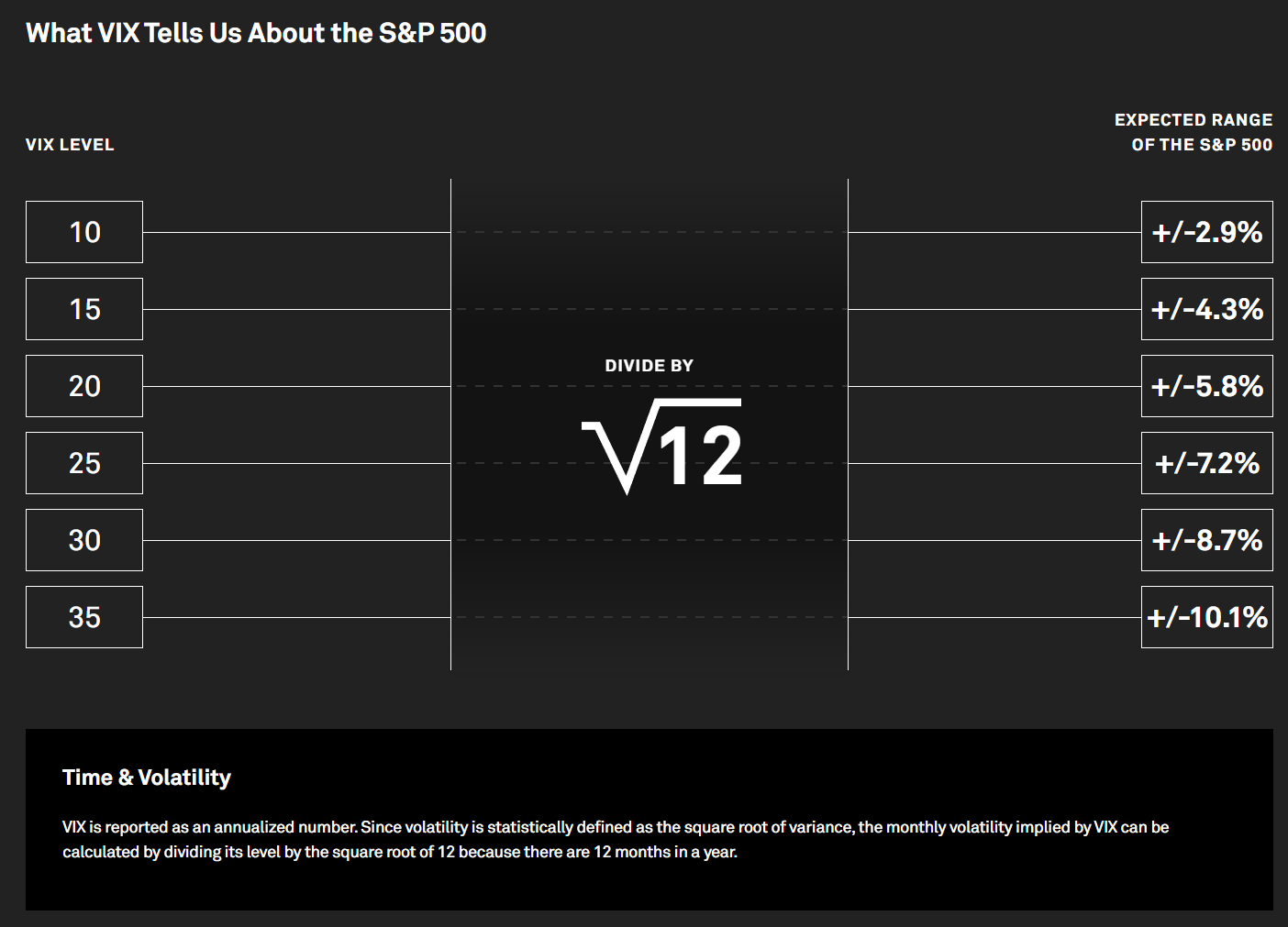

Understanding Market Volatility

Volatility reflects the degree of price movement in financial markets and is often measured using the CBOE Volatility Index (VIX). While short-term traders may see volatility as an opportunity, it often represents heightened risk for long-term investors. Volatility spikes are typically triggered by uncertainty, whether political, economic, or geopolitical, and can lead to significant portfolio drawdowns if not managed properly.

Key Drivers of Volatility

Economic Uncertainty: Inflation, rising interest rates, and recession fears can destabilize markets.

Political Transitions: Events like presidential inaugurations or changes in government leadership often lead to market jitters.

Geopolitical Tensions: Trade disputes, wars, or supply chain disruptions exacerbate uncertainty.

Market Sentiment: Shifts in investor confidence, often amplified by speculative trading, can lead to sharp sell-offs.

Understanding and recognizing these drivers is crucial for adopting a defensive approach and preparing portfolios to withstand periods of heightened market stress.

Historical Safe-Haven Sectors and Industries

During times of volatility, certain sectors of the market have historically shown resilience. These “defensive” sectors are characterized by consistent demand for their products and services, regardless of economic conditions.

1. Consumer Staples ( XLP 0.00%↑ )

Consumer staples include companies that produce essential goods like food, beverages, and household products. These items remain in demand even during economic downturns, making this sector a traditional safe haven.

Examples of Top Companies: Procter & Gamble ( PG 0.00%↑ ), Coca-Cola ( KO 0.00%↑ ), PepsiCo ( PEP 0.00%↑ ).

Caution: As demonstrated by recent trends, Consumer Staples are not entirely immune to sell-offs, particularly when broader market sentiment deteriorates or defensive sectors are themselves over-valued.

2. Healthcare ( XLV 0.00%↑ )

Healthcare is another defensive sector, as people require medical services and pharmaceuticals regardless of the economy's state. This sector benefits from stable cash flows and growth opportunities, particularly with an aging population driving demand.

Examples of Top Companies: Johnson & Johnson ( JNJ 0.00%↑ ), Pfizer ( PFE 0.00%↑ ), UnitedHealth Group ( UNH 0.00%↑ ).

3. Utilities ( XLU 0.00%↑ )

Utilities, such as electricity and water providers, are considered defensive due to the essential nature of their services. These companies often offer reliable dividends, further enhancing their appeal during market turbulence.

Examples of Top Companies: NextEra Energy ( NEE 0.00%↑ ), Duke Energy ( DUK 0.00%↑ ), Dominion Energy ( D 0.00%↑ ).

4. Real Estate Investment Trusts (REITs)

REITs focused on residential housing and healthcare facilities tend to perform well during economic slowdowns. They provide a stable income through dividends and often hold up better than other real estate sectors during market downturns.

Examples of Top REITs: Public Storage ( PSA 0.00%↑ ), American Tower ( AMT 0.00%↑ ).

5. Precious Metals

Gold and silver are classic safe-haven assets. Investors often turn to these commodities during periods of uncertainty to preserve value and hedge against inflation.

Top Instruments: SPDR Gold Shares ( GLD 0.00%↑ ), iShares Silver Trust ( SLV 0.00%↑ ). There are many other ETFs for precious metals however:

By diversifying into these sectors, investors can reduce portfolio volatility while maintaining exposure to essential industries.

Portfolio Instruments to Mitigate Volatility

Even with sector diversification, specific financial instruments are necessary to manage portfolio risk effectively. These tools are designed to preserve capital, hedge against losses, and provide liquidity.

1. Cash and Cash Equivalents

Holding cash or cash equivalents, such as Treasury bills or money market funds, provides liquidity and preserves capital. This enables investors to redeploy funds into the market when conditions improve.

2. Bonds

Bonds offer stability and consistent income, acting as a counterweight to equities during volatile periods.

Treasuries: U.S. government bonds are considered risk-free and offer predictable returns.

Municipal Bonds: Provide tax advantages and relatively low risk for high-income investors.

Corporate Bonds: Investment-grade bonds deliver higher yields with moderate risk.

3. Hedging with Derivatives

Derivatives provide a way to protect portfolios without selling underlying assets.

Put Options: Act as insurance by giving the holder the right to sell at a predetermined price.

Covered Calls: Generate income while slightly reducing risk.

Futures Contracts: Hedge exposure to commodities, currencies, or indices.

4. Inverse ETFs & Volatility ETFs

Inverse ETFs allow investors to profit from market declines, offering a hedge against falling markets.

Examples: ProShares Short S&P 500 ( SH 0.00%↑ ), ProShares UltraShort QQQ ( QID 0.00%↑ ). There are many liquid options available for you to choose from:

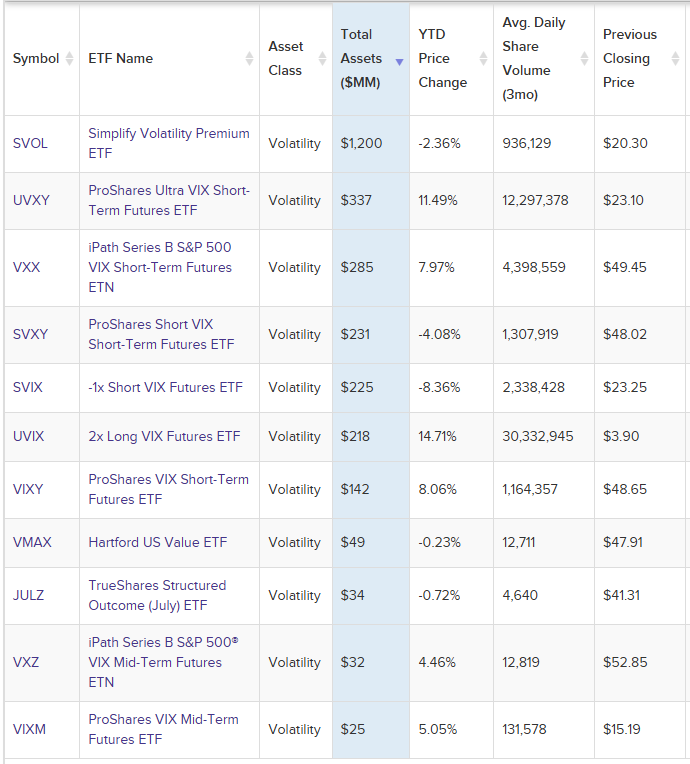

There are also several ETFs that track volatility offering investors ways to hedge against downturns or even profit from them:

5. Low-Volatility ETFs

Low-volatility ETFs aim to reduce risk while maintaining equity exposure.

Examples: iShares MSCI USA Minimum Volatility ETF ( USMV 0.00%↑ ), Invesco S&P 500 Low Volatility ETF ( SPLV 0.00%↑ ).

6. Commodities

Beyond precious metals, broader commodity exposure can act as a hedge against inflation and economic downturns. Here’s a short list of some of the most liquid ETFs in this space as an illustration of what is available:

Strategies to Preserve Cash for Redeployment

Preserving cash and maintaining liquidity during market downturns is essential. This enables investors to capitalize on opportunities when valuations become more favorable.

1. Rebalancing Portfolios

Reviewing and adjusting allocations by shifting from high-risk growth stocks to defensive sectors or fixed-income instruments can reduce portfolio risk.

2. Stop-Loss Orders

Stop-loss orders automate selling when an asset's price falls below a predetermined level, limiting your downside risk.

3. Dividend-Paying Stocks

Investing in companies with a history of consistent dividends provides income and stability during downturns.

4. Tactical Asset Allocation

Tactical allocation involves dynamically adjusting portfolio composition based on market conditions, prioritizing defensive assets during periods of volatility.

Lessons from Historical Volatility Events

Examining past periods of heightened volatility provides valuable lessons for defensive investing.

Case Study 1: The 2008 Financial Crisis

Defensive sectors like Consumer Staples and Healthcare outperformed growth sectors.

Bonds and gold emerged as reliable hedges.

Key takeaway: Defensive assets preserved value while the broader market suffered significant losses.

Case Study 2: COVID-19 Market Crash (2020)

Technology and Healthcare rebounded quickly, while Energy and Financials lagged.

Diversification across defensive sectors helped mitigate losses.

Key takeaway: Flexible and diversified strategies proved most effective.

Conclusion

Navigating volatile markets requires discipline, a clear understanding of risk, and the right tools. Defensive investing is not about avoiding risk entirely but about positioning portfolios to withstand downturns while preserving the potential for future growth.

By focusing on historically resilient sectors, incorporating risk-mitigating instruments, and adopting prudent strategies to preserve cash, investors can weather turbulent times and emerge stronger. While no strategy is foolproof, a defensive approach tailored to individual risk tolerance and financial goals can provide the stability and confidence needed to stay the course.

In an environment poised for volatility, adopting a defensive mindset ensures not only the preservation of capital but also the readiness to seize opportunities when the market eventually stabilizes - be prepared to lean into pullbacks as opportunities to diversify and add quality investments at discounted prices across multiple corners of the market.